Audit Report of the Participant Funding Program

Table of contents

- EXECUTIVE SUMMARY

- 1 BACKGROUND

- 2 AUTHORITY

- 3 OBJECTIVE, SCOPE AND APPROACH

- 4 STATEMENT OF CONFORMANCE

- 5 ACKNOWLEDGMENT

- 6 FINDINGS AND OBSERVATIONS

- 7 OVERALL CONCLUSION

- 8 MANAGEMENT ACTION PLAN

- Appendix A Audit Criteria

- Appendix B PFP Milestones Timeline

- Appendix C Categories of PFP Funding Activities

- Appendix D Financial Data

- Appendix E Acronyms

EXECUTIVE SUMMARY

The objective of the Participant Funding Program (PFP) audit was to provide reasonable assurance that management controls were in place and that the PFP was executed in compliance with Canadian Nuclear Safety Commission (CNSC) processes and guidelines, with its own terms and conditions (T&Cs), and with applicable Treasury Board (TB) policies over the scope period of fiscal years 2019–20 and 2020–21.

Why this is important

The CNSC established the PFP to encourage individuals, not-for-profit organizations and Indigenous groups to participate in the CNSC’s environmental assessment (EA) and licensing processes for major nuclear facilities, and to assist with bringing value-added information to Commission proceedings.

Since the PFP was established in 2011, there have been expansions to its categories as well as a steady increase in demand for funding, which has resulted in funding pressures on the CNSC. In 2019–20, the demand for participant funding exceeded the TB-allocated funding for the first time in the history of the PFP. The same occurred in 2020–21, and trending suggests this is likely to occur in future years as well.

A key priority area for the CNSC is the implementation of trust and reconciliation strategies, which includes building trust with all stakeholders and supporting Indigenous reconciliation through outreach and engagement at Commission proceedings. The Reconciliation Strategy supports the CNSC’s comprehensive Trust Building Strategy by considering the political, legal and policy context within which the CNSC must work and collaborate with Indigenous groups. The PFP supports these strategies, as it is a mechanism for assisting individuals, not-for-profit organizations and Indigenous groups in bringing value-added information to the Commission, thus playing a role in moving these strategies forward.

Key findings

The audit found that several different areas of the CNSC have roles and responsibilities tied to the PFP, including the Finance and Administration Directorate (FAD), Legal Services (LS) and the Commission Secretariat. The CNSC would benefit from additional internal alignment, including a clear and documented outline of responsibilities to establish a consistent, mutual understanding of the PFP as it currently stands and going forward.

Given that the long-term financial sustainability of the PFP remains uncertain should demand for its services continue to increase, the PFP should provide the Integrated Planning and Resource Management Committee (IPRMC) with options to clarify the strategic direction and funding categories for IPRMC’s decision, and should explore opportunities to revisit the PFP envelope over the long term.

PFP processes have been developed to ensure effective management. However, there are opportunities to update some processes that have changed since the inception of the PFP. A file review showed that, overall, transactions were complete and consistent with PFP internal procedures, and all funding awarded was linked to specific Commission proceedings.

While there are processes in place for regular PFP risk reporting and financial monitoring, ongoing and active tracking and reporting of PFP performance against its intended outcomes is not performed in line with the PFP’s TB submission requirements; only a limited assessment of program effectiveness and relevance is performed.

The audit includes 4 recommendations aimed at addressing the above-noted areas for improvement.

Management agrees with the recommendations, and its responses demonstrate its commitment to taking action.

1 BACKGROUND

Purpose

The CNSC regulates the use of nuclear energy and materials to protect the health, safety and security of Canadians and the environment, and to implement Canada’s international commitments on the peaceful use of nuclear energy.

Whenever a major licensing decision for a nuclear facility or activity needs to be made, the CNSC holds a public Commission hearing. During these hearings, the Commission – an independent administrative tribunal set up at arm's length from government – considers written and oral statements from CNSC staff, the licensee or applicant, and the public before making a decision.

History and structure of the PFP

The PFP is intended to improve the regulatory review process for nuclear projects. Specifically, the CNSC established the PFP to encourage individuals, not-for-profit organizations and Indigenous groups to participate in the CNSC’s EA and licensing processes for major nuclear facilities, as well as to assist these same groups in bringing value-added information to the Commission through informed and topic-specific interventions related to EAs and licensing.

Canada’s 2010 federal budget gave the CNSC the authority to create the PFP, which was established in 2011–12 from the associated approved TB submission. The TB submission laid out the initial risk assessment and performance measures that the PFP was required to monitor and report on in order to operate. In addition, the TB submission included the approved funding budget, source of funds, and T&Cs for the PFP.

In 2013, and again in 2016, the CNSC’s Management Committee approved new funding categories for the PFP (see appendix B). The expansion categories support meetings that provide value-added information to the Commission (see appendix C).

In order to be considered for funding, PFP applicants have to demonstrate that they have relevant information to contribute to specific PFP funding opportunities. An independent funding review committee (FRC), composed of a panel of external experts, reviews funding applications prior to a contribution amount being determined. The PFP is committed to gathering feedback at the end of each Commission proceeding in order to determine whether the interventions provided value-added information.

The Indigenous and Stakeholder Relations Division (ISRD), within the Strategic Planning Directorate (SPD), manages the PFP. The ISRD supports relationship building with the public and Indigenous peoples through the dissemination of scientific and project-related information and by encouraging public participation and Indigenous consultation in the CNSC's regulatory processes. The ISRD is also responsible for the Trust Building Strategy and the Reconciliation Strategy, including outreach and engagement in relation to Commission proceedings.

The PFP’s annual budget of $925,000 cannot be used for non-transfer-payment activities, and any spending in excess of the $925,000 must be funded by lapsing appropriation funds. The funds are fully recovered from regulated parties, with no net impact on the fiscal framework.

The CNSC cost recovers PFP expenditures through the Regulatory Activity Plan (RAP) fee process. RAP fees are calculated by applying a proportional costing methodology that allocates all expenditures, including PFP expenditures, based on the CNSC’s planned direct effort in relation to each RAP fee-paying licensee. This model was implemented following the licensees’ request for more predictability in their fees. In order to fully recover PFP costs, a year-end manual adjustment to RAP fees is performed to allocate the PFP’s actual expenses based on the year-end proportional percentages.

In 2019–20, the PFP awarded a total of $1,125,192 to 88 recipients, of which 51 were Indigenous communities or organizations. This was the first year that the CNSC overspent the amount allocated to the PFP by TB. In 2020–21, the PFP disbursed $1,109,137 to 86 recipients and is forecasting that the demand for funding will continue to grow in subsequent years. Additional financial data demonstrating the increase in demand for participant funding since the creation of the PFP in 2011 up to the present can be seen in appendix D.

2 AUTHORITY

This audit was authorized through the 2020–23 Risk-Based Audit Plan, which was revised and approved by the President and CEO of the CNSC on October 27, 2020.

3 OBJECTIVE, SCOPE AND APPROACH

The objective of the PFP audit was to provide reasonable assurance that management controls were in place and that the PFP was executed in compliance with CNSC processes and guidelines, with its own T&Cs, and with applicable TB policies for the audit scope period of fiscal years 2019–20 and 2020–21.

The audit lines of inquiry and criteria are set out in detail in appendix A.

4 STATEMENT OF CONFORMANCE

This internal audit was conducted in conformance with the International Standards for the Professional Practice of Internal Auditing, and in accordance with the requirements of the TB Policy on Internal Audit and Directive on Internal Audit, which set out mandatory procedures for internal auditing in the Government of Canada.

5 ACKNOWLEDGMENT

The audit team would like to acknowledge and thank management and staff for their support throughout the conduct of this audit.

6 FINDINGS AND OBSERVATIONS

6.1 Governance Framework

A governance framework is a set of rules and practices by which an organization ensures accountability, fairness and transparency with all its stakeholders. Given the various internal and external stakeholders involved in any contribution program, having a clearly defined and integrated governance structure is key to ensuring that program outcomes are achieved.

Governance

The audit expected to find governance structures in place to support the PFP, including internal governance structures supporting the PFP with documented and communicated roles, responsibilities and accountabilities.

The PFP reports to the IPRMC on a regular, periodic basis. The IPRMC's primary purpose is to ensure the optimal allocation of all CNSC resources in order to achieve desired outcomes in both the long term and the current fiscal year, in line with the CNSC's vision. To support this mission, the IPRMC is chaired by the President and CEO of the CNSC, and includes all Executive Committee members as well as director general–level representatives from across the organization. As of September 2019, the PFP has begun to report quarterly to the IPRMC for the main purpose of financial monitoring.

The ISRD manages the PFP, while FAD supports financial operations related to the PFP. Similarly, LS provides legal support, where required. Other areas of the organization also perform work related to the PFP, including the Commission Secretariat, which provides Commission feedback on the value-added nature of PFP outputs.

Management system documentation, including roles and responsibilities, was prepared in 2013. However, it is no longer completely aligned with the current situation, as it references committees and divisions that no longer exist. For example, the documentation refers to an internal review committee with representatives from all the affected business areas related to a project. The audit found that the PFP internal review committee was never officially established. Instead, in addition to the external FRC’s input, the PFP administrator engages with the project officer/EA officer, Secretariat and Communications on each funding opportunity for input, as required. The Commission Secretariat also schedules a meeting with relevant internal partners related to the PFP for each proceeding. As a result, there is an opportunity to improve the clarity and understanding of roles and responsibilities and to review and communicate a shared understanding of roles and responsibilities through updated documentation.

Through interviews, the audit found that representatives from these internal stakeholder areas did not always have a clear understanding of the PFP, specifically its scope and funding mechanisms, especially given the PFP expansions over the years.

Before 2018, the PFP team engaged with internal stakeholders and provided presentations at various divisional meetings on PFP expansion. However, those efforts have not continued.

The audit found that there is an opportunity for additional internal alignment, including a clear and documented outline of responsibilities, to establish a consistent, mutual understanding of the PFP. Without effective alignment, the different internal stakeholder areas may be unaware of each other’s work with respect to the PFP, which may lead to gaps or duplication of effort.

Strategic Planning

Since the PFP was established in 2011, its categories have been expanded and there has been a steady increase in requests for contribution funding. In 2019–20, the demand for contribution agreement funding exceeded the PFP’s TB funding authorities for the first time. The PFP has forecasted that this trend will continue (see appendix D).

The audit conducted a benchmarking study and found that other government departments with similar PFPs have amended their programs in recent years by seeking TB approval for additional funding to support increased collaboration with Indigenous groups. During the course of the audit, the PFP was working on long-term forecasting to determine whether a similar program requirement existed within the CNSC.

In 2019, the Government of Canada introduced the Impact Assessment Act (IAA), which provided new and updated legislation on the conduct of impact assessments (IAs) to assess the environmental, economic, social and health impacts of projects, the gender-based impacts, and the effects on Indigenous peoples’ rights. The IAA also created the Impact Assessment Agency of Canada (IAAC). Subsequently, the CNSC signed a memorandum of understanding with the IAAC to confirm that the CNSC would follow a distinct process for nuclear assessments and that guidance for participants would be developed in order to implement an overarching framework that would allow for a single process for integrated IAs. While the current process does not impact the PFP, it may be important for the CNSC to monitor the impact of the implementation of the IAA on the PFP.

As stated in the CNSC’s 2020–21 Departmental Plan, one of the priority areas for the CNSC is implementing trust and reconciliation strategies, which includes building trust with all stakeholders and supporting Indigenous reconciliation through ongoing outreach and engagement. The CNSC’s Reconciliation Strategy supports the CNSC’s comprehensive Trust Building Strategy by considering the political, legal and policy context within which the CNSC must work and collaborate with Indigenous groups. The PFP supports these strategies, as it is a mechanism for assisting individuals, not-for-profit organizations and Indigenous groups in bringing value-added information to the Commission, thus playing a role in moving these strategies forward.

Over the course of the audit, the CNSC had been considering different approaches to supporting its Reconciliation Strategy. Aspects of this strategy may need to be considered when looking at longer term trends and the budget of the PFP.

Current forecasts suggest that demand for the PFP’s services will continue to grow significantly (see appendix D). As a result, the CNSC will have to continue to make decisions on whether to reallocate funds from within the organization to account for any overages in the amount required by the PFP above TB authorities. A financial assessment of the long-term potential operational impact to other programs and operations to cover these additional costs has not yet been completed (see section 6.3 for more information on expenditure authorities).

Conclusion

The PFP, while housed within SPD, touches on a number of other areas within the CNSC. The PFP’s governance and reporting mechanism is clear and is being used as expected, however, the CNSC would benefit from additional internal alignment among key stakeholders. This would support greater understanding of the PFP itself, as well as the possibility for more integrated, holistic approaches across the CNSC, supporting the strategic goals of the organization and avoiding gaps or duplication across implicated internal stakeholders and strategies.

Recommendation 1: The Strategic Planning Directorate, in collaboration with the Finance and Administration Directorate, Legal Services and Secretariat, should identify, document and communicate each of the internal stakeholder areas’ roles, responsibilities and accountabilities related to the Participant Funding Program.

Recommendation 2: The Strategic Planning Directorate should provide the Integrated Planning and Resource Management Committee with Participant Funding Program options to clarify the strategic direction and funding categories for IPRMC’s decision, and should explore opportunities to revisit the PFP envelope over the long term.

6.2 Risk Management, Processes and Controls

Risk management supports organizations in making informed decisions for allocating resources, mitigating threats, and proactively capitalizing on opportunities.

Policies and processes are critical in ensuring consistency in the way contribution programs are managed and applied. They should be aligned with the governance framework and risk management process, and should support management and staff in discharging their responsibilities according to expectations.

Risk Management

The CNSC’s Enterprise Risk Profile (ERP) is designed to assess and respond to risks that may act to constrain or limit the organization's successful achievement of its mandate. While ISRD does not conduct a separate risk assessment, it contributes to the ERP, which includes a risk related to Indigenous engagement and consultation. This was ranked as a high-risk area due to the lack of CNSC capacity and resources to manage growing expectations and the volume of consultations and workload in this area.

As part of the documentation to support the quarterly PFP presentation to the IPRMC, program risks are integrated within the presentation. While a discussion and assessment of the funding risk is the main purpose of the presentation, embedded in the documentation is risk monitoring, which is a good practice.

As part of the approved TB submission, the PFP completed a risk assessment and mitigation strategy, documenting 2 high risks at the time, both of which the PFP committed to mitigating. Firstly, in order to mitigate the risk of the perception of bias with an internal funding committee, the PFP put in place an FRC consisting of external members. The FRC serves as a challenge function for funding requests and recommends the funding to be allocated for each request. Secondly, the risk of the impact of project delays due to management of the PFP was mitigated through the development of timelines for each type of project for which participant funding could be available, the creation of templates and tools to enhance the effectiveness of the PFP, and the elimination of complex contribution agreements and applications to minimize assessment time.

The risk management model was developed in 2013 to address PFP processes and was updated in 2015 to address 2 of the 3 expanded PFP categories. The PFP would benefit from updating the model to include all the expanded categories.

Compliance with Processes

The CNSC is subject to the TB Policy on Transfer Payments and related instruments. The policy requires transfer payment programs to be designed, delivered, and managed in a manner that is fair, accessible, and effective for all. The audit found that the funding decisions and contribution agreement preparations were documented in accordance with the PFP’s T&Cs and in compliance with the TB Policy on Transfer Payments and its related directive.

The audit found that all the required information to apply for funding was available on the CNSC’s website, in both official languages. The website also provided the public with details on the funding processes, including direct access to corresponding guides and templates, which is a good practice.

The audit included the review of a sample of PFP files to assess whether the PFP was executed in compliance with established processes and guidelines. Testing of the sample concluded that:

- PFP transactions were complete and consistent, in accordance with established processes and guidelines

- PFP applications were reviewed and selected against eligibility criteria, as defined in the T&Cs

- PFP applications were reviewed by the FRC, which performed an effective challenge function

- PFP payments were awarded to recipients that fell within the definition of eligible PFP applicants

- PFP contributions were aligned with PFP objectives, and the requested funding fell within the scope of eligible expenses

- Recipient audits of payments over a specified threshold were conducted

- Contribution agreements were signed before the release of funding in all cases

The audit did note that the processes and procedures documents were not always correctly linked to the PFP guide. As the PFP expanded, new tools, templates and guides were developed that did not necessarily correctly link to the original documents created.

During the course of the audit, the division managing the PFP was reorganized in response to broader organizational requirements, with the division title changing from the Policy, Aboriginal and International Relations Division to the Indigenous and Stakeholder Relations Division. As a result, documentation will need to be refreshed to align with the new divisional name.

The audit also found that there were opportunities to review and update processes developed at the PFP’s inception, given that it is now over 10 years old. While this did not have an impact on compliance with the PFP’s requirements as per the results of testing, there is an opportunity to modernize and refresh process documents.

Lastly, while the participant guide requires all recipients of PFP funding to complete a satisfaction survey, response rates have hovered at under 50% over the years. As the completion of these surveys is outside the control of the PFP given that they must be completed by external parties, there may be an opportunity to clarify expectations. More on recipient surveys can be found in the performance measurement section of this report.

Financial Monitoring

The audit expected to find evidence that, in addition to financial controls, the PFP funding budget is monitored on a periodic, ongoing basis and reported on to management.

As of September 2019, the PFP has been required to provide quarterly updates to the IPRMC. The PFP has made regular presentations to the IPRMC, including an overview of current funding and a historical breakdown of funding by licensee and by year. Contribution funding forecasting and planning, including the forecasted increase in recipient demand, is taking place as well, and is being monitored and reported to the IPRMC. This has included presentations on funding pressures in order for the IPRMC to make resource allocation decisions related to the PFP.

According to interviews, the increase in PFP spending was manageable in 2020–21 as a result of a budget surplus stemming from decreased spending due to the restrictions caused by the global pandemic. In future years, based on the current PFP structure and without a dedicated funding source, the CNSC would have to continue to cash manage and reallocate funds from other programs and operations to account for any overages in the amount required by the PFP above the TB authorities. Current forecasts suggest that PFP demand will continue to grow significantly, rising from $1.1 million in actual spending in 2020–21 to over $2 million in forecasted demand for 2021–22. As a result, the risk and potential impact to other areas of the CNSC continues to grow.

An assessment of the potential operational impact to other programs and operations from having to cover the costs of the overages in PFP funding levels above its allocated authority has not yet been completed. Furthermore, no such assessment was completed in either 2013 or 2016, when the PFP was expanded. Thus, while the funding risks are brought forward to the IPRMC, the long-term financial sustainability of the PFP and potential impacts on the CNSC as a whole remains unassessed.

Indirect PFP costs

While historical, actual and forecasted contribution funding is being actively monitored and reported to senior management, indirect costs related to program administration, while monitored, are not included in the reporting to senior management.

The approved TB submission that provided authority for the PFP allocated $175,000 annually to cover indirect costs (salary, operating and maintenance costs, travel, communications, translation, and professional fees for the FRC).

The TB submission indicated that the portion of indirect costs was expected to decrease over time “as experience is gained with the program and once start-up costs are no longer required. However, this is likely to be offset by an increased number of applicants as knowledge of the funding program grows through time.”

The internal program costs have historically been much lower than the total budget allocated through the TB submission, averaging at around $42,000 of the $175,000 annual budget. The CNSC has reallocated the excess of the indirect costs to funding programs outside the PFP. This falls within the purview of the CNSC, as indirect costs are internally funded. However, there may be an opportunity to reallocate these costs to the PFP in order to support the increased number of applicants, as per the TB submission’s intent.

Conclusion

Overall, risk management of the PFP is conducted and reviewed through the ERP on an annual basis. Risk documentation could be updated to reflect all currently approved funding categories.

Processes have been developed to ensure effective management of the PFP. However, there are opportunities to update some of these processes. A file review showed that, overall, PFP transactions are complete and consistent with procedures.

Consistent financial monitoring and reporting is also conducted for contribution expenditures and forecasts. However, the long-term financial impacts resulting from the need to make internal reallocations from other areas within the CNSC to meet the PFP budget overages, and the resulting impacts on other areas within the CNSC, need to be considered, especially given the expected rise in funding requests in future years. This may also be helpful in determining whether changes may be required to the PFP’s expenditure authorities to ensure its long-term viability (section 6.3 of this report provides more information on expenditure authorities).

Recommendation 3: The Strategic Planning Directorate should update process documents, tools and templates (including risk-management documentation).

6.3 Program Authority

Statutory authorities are the expenditure authorities approved by Parliament through legislation (other than appropriations acts). The legislation under which these authorities are given sets out the purpose of the expenditures and the terms and conditions under which they may be made.Footnote 1

Expenditure authorities are approvals from Parliament for individual government organizations to spend up to specific amounts. Expenditure authority from Parliament is provided in 2 ways: in the form of annual appropriations acts that specify the amounts and broad purposes for which funds can be spent, or in the form of other specific statutes that authorize payments and set out the amounts and time periods for those payments. An organization’s expenditure authority received through appropriations acts may be supplemented by allocations from other TB Central Votes.Footnote 2

The CNSC derives the statutory and expenditure authorities to execute and fund the PFP through the Nuclear Safety and Control Act (NSCA), which states in paragraph 21(1)(b.1) that “The Commission may, in order to attain its objects, establish and maintain a participant funding program to facilitate the participation of the public in proceedings under this Act”, and through the PFP’s approved TB submission.

Statutory Authority

The audit expected to find evidence that the PFP is in compliance with the statutory authority granted to it through both the NSCA and the PFP’s approved TB submission and associated policies, regulations and T&Cs.

The TB submission that led to the creation of the PFP outlined the categories of eligible PFP activities (see appendix B). In 2013, Management Committee approved 2 new categories in addition to the original 3 categories described in the TB submission: support for meetings with Indigenous groups on matters of regulatory concern, and participation in CNSC targeted studies and monitoring.

Subsequently, in 2016, Management Committee approved an additional 3 categories: review of discussion papers, regulatory documents and regulations; long-term Indigenous engagement meetings and activities; and participation of Indigenous communities in environmental monitoring, including the Independent Environmental Monitoring Program (IEMP).

In 2013, a legal review concluded that “on a case-by-case assessment, the CNSC may establish a PFP for the participation of the public or Aboriginal peoples in circumstances, such as CNSC outreach or engagement activities, where these activities are reasonably justifiable and directly linked to Commission proceedings and its deliverables would benefit and provide value to Commission proceedings.” During the planning phase of the audit, a risk was identified that any PFP expansions risked being outside legislative authorities if there were no longer a sufficiently close connection linking some types of funding agreements to Commission proceedings, particularly those related to general matters of regulatory interest and the Crown’s constitutional duty to consult. This would in turn affect the funding mechanism used to support these types of requests (cost recovery–based versus appropriations-based).

The PFP T&Cs were written to be flexible and allow for a wide variety of activities to be funded. However, the premise of the PFP was to have a connection between the contribution agreements entered into and Commission proceedings, with deliverables directly contributing to specific matters being brought forward to the Commission.

The T&Cs section of the PFP TB submission explicitly describe the non-statutory authorities to be considered eligible for funding under the PFP, which include:

- be an eligible recipient

- conduct an eligible activity

- assist in preparing for and contributing to a better understanding of the issues before the Commission.

PFP funding categories are split between project-specific funding and funding for general matters of regulatory interest (see appendix C). The audit conducted a walk-through of funding applications and found that the PFP is in compliance with the current authorities, as each funding request is linked to a Commission proceeding. The PFP maintains documentation on all PFP contribution agreements and the output that is presented to the Commission.

Expenditure Authority

TB submissions lay out the expenditure authority and funding source for a program or initiative. For the PFP, the funds are fully recovered from regulated parties, with no net impact on the fiscal framework. A proportional costing method is used to allocate all expenditures, including PFP expenditures, based on the CNSC’s planned direct effort in relation to each RAP fee-paying licensee. Fee-paying licensees are invoiced to support the contributions component of the PFP. The amounts are non-respendable revenue for the CNSC and are returned to the Government of Canada Consolidated Revenue Fund.

The audit expected to find that the PFP’s sources of funding were clearly understood across the key internal stakeholder areas that support the delivery of the PFP. However, through interviews, the audit found that there was confusion regarding the PFP funding mechanisms. As noted earlier in the Governance section of the report, there may be an opportunity for greater internal stakeholder alignment to strengthen the understanding of the PFP within the CNSC and support informed decision making.

The audit also expected to find that the PFP was managed within its expenditure authorities. Until 2017–18, the PFP operated under the $925,000 contribution authority granted by its TB submission, and there was a clear understanding of the source of funding, mandate and objectives of the PFP. As a result of the PFP’s expanded categories, there was an increase in contribution spending by 2018–19. At the time, there was a risk that the PFP would go over its funding authority, which was avoided through the deferral of some payments to the next fiscal year.

The audit found that the approval of the PFP’s expanded categories, while appropriately approved by the President and Management Committee, was done without a full assessment of the impact on PFP demand and without a sustainable and predictable additional funding source in the event that the PFP had to go over its funding envelope.

In 2020, SPD and FAD presented 3 different PFP funding options to IPRMC: status quo (RAP fees – proportional costing methodology), directly charging specific RAP fees (or groups of RAPs) to licensees for the participant funding related to their projects, or a fixed model. Through a detailed analysis, IPRMC supported continuing the use of the status quo method of cost recovery for the PFP.

To date, the PFP has only gone over its allocated budget in 2019–20 and 2020–21. However, ISRD is predicting that this trend will continue in the future. In the past 2 fiscal years, the additional funds over the $925,000 financial authority limit have been transferred from other programs and operational areas within the CNSC, with the appropriate IPRMC approval. While the costs are cost-recovered by the CNSC from licensees, the recovered funds go directly into the Government of Canada Consolidated Revenue Fund and are not respendable for CNSC operational requirements, thus creating the possibility that these transfers may cause internal financial pressures if continued in the future.

Conclusion

Based on a sample of files audited, the PFP is currently operating within its statutory, financial and policy authority, given that all approved funding requests are linked to specific Commission proceedings. As noted in section 6.1, there is an opportunity to consider the long-term impacts of other strategies within the CNSC, more specifically the CNSC’s Reconciliation Strategy, to support a holistic and integrated approach for all matters related to reconciliation and the Crown’s duty to consult.

Similarly, as noted in earlier sections, there may be a need to revisit the expenditure authority allocated to the PFP to support its long-term viability.

6.4 Performance Measurement

Performance measurement, including monitoring and reporting, is key to ensuring the successful implementation of a program. Successful performance measurement practices support management oversight and help identify issues or areas for management attention. Performance monitoring of and reporting on contribution agreements is also an essential part of the PFP’s requirements in the TB submission.

TB Submission Performance Measurement Requirements

The audit expected to find documentation supporting the performance measures required by the TB submission.

The first requirement, Measuring Program Outcomes, is measured by assessing the percentage of recipients who agree that the funding provided improved their ability to participate in Commission proceedings. The audit found that the results were reported as part of the annual Departmental Performance Report.

The second requirement, Measuring Program Efficiency, is assessed by the timeliness of the funds received. The audit found evidence of monitoring to measure timely decisions; however, performance measurement data reported on the CNSC’s website has not been updated in over 2 years. These results are out of date and do not reflect that the CNSC is not currently hitting the target of 100% (actuals were 64% in 2019–20 and 84% in 2020–21). While there is reporting as part of the Government of Canada service inventory, this information can be challenging for interested parties to find and is not as accessible through the CNSC’s website.

The logic model serves as a program's road map. It outlines the intended results (i.e. outcomes) of the program, the activities the program will undertake, and the outputs it intends to produce in achieving the expected outcomes. The purpose of the logic model is to:

- help program managers verify that the program theory is sound and that outcomes are realistic and reasonable

- ensure that the performance measurement strategy framework and the evaluation strategy are clearly linked to the logic of the program and will serve to produce information that is meaningful for program monitoring, evaluation and, ultimately, decision making

- help program managers interpret the monitoring data collected on the program and identify implications for program design and/or operations on an ongoing basis

- serve as a key reference point for evaluators in upcoming evaluations

- facilitate communication about the program to program staff and other program stakeholders

The third requirement, Measuring Program Efficiency, is assessed by taking the time frame for making a funding decision and releasing the funding, and comparing it to the time frame set out in service standards. Specifically, the performance measure reads:

“The extent to which recipients received approved funding in a timely manner that allows them to prepare for participation.”

The PFP is measuring the turnaround time for acknowledging the receipt of applications (which is a 1-day service standard). This is a good practice and should continue. However, tracking of this measure does not replace the requirement to track the time it takes to provide funding to ensure that participants have time to adequately prepare for participation. The audit found no evidence that this performance measure is being reported on or that the PFP is tracking this information.

In support of performance measurement, the TB submission also requires the conduct of a program evaluation of the PFP every 5 years. Program evaluations collect and analyze evidence to assess the performance of programs, initiatives and policies in a systematic and neutral way, and consider how programs can be improved. A program evaluation of the PFP was last conducted in 2015, with no immediate plans to conduct a subsequent evaluation. While the 2017 TB Policy on Results states that programs under $5 million are no longer required to be evaluated every 5 years, it would be a good practice to have periodic program evaluations of the PFP.

As part of the evaluation in 2015, the PFP developed a logic model.Footnote 3 This logic model outlines the ultimate, intermediate and immediate intended outcomes of the PFP and serves as the PFP road map. For the PFP, the key outcomes include:

- public confidence in CNSC decisions is maintained / the public is informed on the effectiveness of the regulatory regime (ultimate outcome)

- there is enhanced participation of the public, Aboriginal groups and other desired stakeholders in the CNSC regulatory process (proceedings) (intermediate outcome)

- the Commission is provided with value-added submissions for decision making (intermediate outcome)

- internal stakeholders are aligned on PFP objectives and priorities (immediate outcome)

- desired participant groups are aware of program funding opportunities and process (immediate outcome)

- participants perceive the program to be fair and readily accessible (immediate outcome)

As a best practice, the PFP would ideally be tracking and monitoring its performance against each of its defined intended outcomes. This would typically be in the form of a program performance measurement strategy framework that outlines the outcomes, reporting frequency, data sources and responsibilities. At the time of the audit, the PFP did not have a framework in place to monitor and report against the outcomes listed in the logic model.

Value-Added Reporting

According to PFP process documentation, reporting to determine whether PFP deliverables are adding value to Commission proceedings has always been a part of the PFP’s internal processes.

At a 2018 Management Committee meeting, there was an action item for the Commission Secretariat function to enhance the existing value-added reporting process. While the process for this enhancement has not been documented, based on interviews, the PFP does receive verbal feedback from the Commission Secretariat following Commission proceedings. ISRD gathers this feedback in order to determine whether the interventions by participant funding recipients were value-added to the Commission hearing, and then creates value-added reports that are shared with FRC members.

The audit reviewed a sample of value-added reports completed after 2018 to determine whether the reports were consistently completed and shared with the FRC, and found that this was the case. In addition, through interviews with the FRC, members noted that these reports are considered before recommending future funding opportunities to the CNSC and are viewed as valuable.

Recipient Surveys

The PFP has designed recipient surveys for participants to complete. The survey questionnaire is meant to reflect key areas of feedback that would be beneficial to the CNSC in terms of improving Commission proceedings and the PFP.

The recipient survey template reviewed does not reflect the expanded range of PFP activities, including the use of the PFP for meetings with Indigenous groups. As a result, feedback on the results and benefits of these expanded activities is not being explicitly sought.

In some cases, as a best practice, the PFP did have recipient feedback notes, which were maintained on file and were well detailed. However, results from surveys are not being actively reported to management and there is no evidence to demonstrate how the results are being rolled up, analyzed and used to support the improvement of the PFP.

The audit found that, despite the fact that section 5.4 of the participant funding guide for funding applicants indicates that the completion of recipient surveys is a requirement, only approximately 50% of recipients submitted the survey to the CNSC during the scope period. SPD has clarified that the completion of the recipient surveys is not a requirement for payment. The audit team also recognizes that the completion of recipient surveys is outside the control of the PFP. However, both the participant guide and website state that the completion of surveys is a recipient requirement; SPD may wish to consider whether this is a feasible requirement.

Conclusion

Overall, there is a lack of complete and consistent monitoring and reporting to support the effective performance measurement of the PFP. Specifically, the audit found opportunities for improvement in order to meet the TB submission requirements for performance measurement and reporting.

SPD should consider updating the applicant funding guide to ensure that it is clear and consistent with the PFP’s requirements and processes.

Without a consistently applied performance measurement strategy, key performance measures are not being monitored and reported on, as required. There is also an opportunity to leverage recipient survey data as well as best practices for a complete performance strategy.

Recommendation 4: The Strategic Planning Directorate should develop and implement a performance measurement strategy that outlines how the Participant Funding Program will ensure that it is monitoring and reporting on requirements, including, but not necessarily limited to, the PFP’s Treasury Board submission requirements.

7 OVERALL CONCLUSION

Based on the results, the audit concluded that while improvements are required to fully meet the audit criteria, there is evidence that processes are in place to support the PFP overall, and that they are working effectively in compliance with the PFP’s T&Cs. However, as the demand for participant funding grows, the PFP will need to work with intradepartmental and interdepartmental partners to determine a sustainable long-term operating model. In addition, a performance measurement strategy that is consistently monitored and reported on would support the effectiveness and efficiency of the PFP and demonstrate its performance against PFP outcomes.

The successful implementation of the recommendations identified in this report, along with the completion of other initiatives already underway by management, will strengthen CNSC management of the PFP. A management action plan to address this audit’s recommendations can be found in section 8.0.

8 MANAGEMENT ACTION PLAN

| Audit recommendation | Risk ranking* | OPI | Management action plan (MAP) | Targeted completion date |

|---|---|---|---|---|

| 1. The Strategic Planning Directorate, in collaboration with the Finance and Administration Directorate, Legal Services and Secretariat, should identify, document and communicate each of the internal stakeholder areas’ roles, responsibilities and accountabilities related to the Participant Funding Program. | Moderate | SPD (FAD, LS) |

SPD agrees with this finding. The roles, responsibilities, and accountabilities of internal stakeholders in relation to the PFP are listed in section 2.0 of each existing PFP process document. SPD will review section 2.0 of each process document and update the text where appropriate. SPD will then share the updated text with the management of each identified internal stakeholder group to re-confirm their roles and responsibilities. Furthermore, SPD will explore opportunities to continue to build awareness of the PFP’s objectives and plans to ensure there is alignment between directorates within the CNSC. This will include utilizing communication tools such as preparing an internal synergy article, attending Divisional and Team meetings with interested divisions upon request, presenting an update at a Management Committee (MC) meeting, and ensuring that program plans continue to be communicated with internal stakeholders such as FAD during monthly meetings with SPD. |

November 30, 2022 |

| 2. The Strategic Planning Directorate should provide the Integrated Planning and Resource Management Committee with Participant Funding Program options to clarify the strategic direction and funding categories for IPRMC’s decision, and should explore opportunities to revisit the PFP envelope over the long term. | Moderate | SPD | SPD agrees with this finding. Starting in Summer 2021, at the direction of IPRMC, SPD has articulated a new strategic program (Indigenous Stakeholder Capacity Program), pending budgetary approval, that will respond to concerns about effective use of PFP funds as well as seek authority to expand the current PFP funding envelope. When SPD is informed of the government’s decision, SPD will return to IPRMC/MC to present and seek approval on the strategic direction of the PFP going forward, including funding categories and the PFP envelope. | October 30, 2022 |

| 3. The Strategic Planning Directorate should update process documents, tools and templates (including risk-management documentation). | Moderate | SPD | SPD agrees with this finding and commits to updating the PFP’s process documents, tools, and templates by November 30, 2022. | November 30, 2022 |

| 4. The Strategic Planning Directorate should develop and implement a performance measurement strategy that outlines how the Participant Funding Program will ensure that it is monitoring and reporting on requirements, including, but not necessarily limited to, the PFP’s Treasury Board submission requirements. | Moderate | SPD |

SPD agrees with this finding. First, the audit found that the program was not adequately tracking one of its TB sub performance measures concerning the timely issuance of payments to recipients. SPD has already commenced working with FAD, to use a similar approach to that of the CNSC’s Research Program, to better document the tracked dates on release of payments which will ensure the PFP is in full compliance with the PFP TB sub requirements. (To be completed by April 2022) Second, SPD has already updated the CNSC’s public website with the latest PFP performance measurement results, which includes results confirming the timely release of contribution agreements to recipients. SPD will also continue the good practice of benchmarking its performance measurement strategy with the Impact Assessment Agency and Canada Energy Regulator. SPD will take a broader look at integrating the performance measurement results in an upcoming meeting to IPRMC and/or Management Committee to better communicate to senior management and staff on how the program is performing. (To be completed by November 30, 2022) |

1) April 1, 2022 & 2) November 30, 2022 |

*Audit recommendations are risk rated as follows:

|

High |

Controls are not in place or are inadequate. |

| Compliance with legislation and regulations is inadequate. | |

| Important issues are identified that could negatively impact the achievement of program/operational objectives. | |

|

Moderate |

Controls are in place but are not being sufficiently complied with. |

| Compliance with central agency/departmental policies and established procedures is inadequate. | |

| Issues are identified that could negatively impact the efficiency and effectiveness of operations. | |

|

Low |

Controls are in place but the level of compliance varies. |

| Compliance with central agency/departmental policies and established procedures varies. | |

| Issues identified are less significant, but opportunities that could enhance operations exist. |

Appendix A Audit Criteria

LINE OF Inquiry 1: Processes are in place to support PFP compliance

1.1 The PFP is in compliance with the current legislative environment, applicable TB policies, and its own T&Cs.

1.2 PFP applications are reviewed and selected against eligibility criteria, as defined in the T&Cs.

1.3 PFP payments are awarded to recipients in compliance with the T&Cs.

1.4 PFP recipient audits are performed as defined in the T&Cs.

LINE OF Inquiry 2: Financial management processes are in place to support the PFP

2.1 The PFP’s sources of funding, mandate and objectives are clearly understood across the key divisions that support the delivery of the program.

2.2 The PFP funding budget is monitored on a periodic, ongoing basis for management.

LINE OF Inquiry 3: Risk and performance management processes are in place to support the PFP

3.1 PFP risks are monitored and mitigated.

3.2 PFP performance results are monitored and reported to senior management.

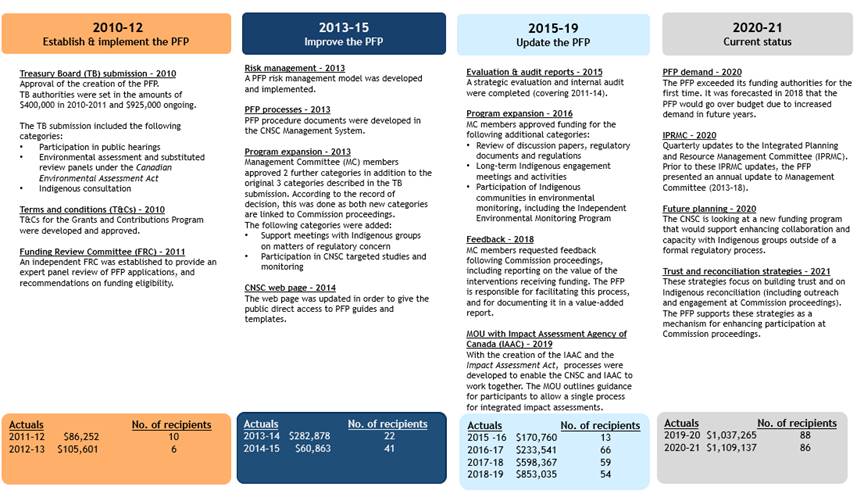

Appendix B PFP Milestones Timeline

Text version

A table with four rows explaining the development of the Participant Funding Program. Each row has a timeline of specific years that explains major events or changes in the Participant Funding Program.

First row 2010-12: “Establish and implement the PFP” (Participant funding program)

Treasury Board (TB) submission – 2010

Approval of the creation of the PFP. TB authorities were set in the amounts of $400,000 in 2010-2011 and $925,000 ongoing.

The TB submission included the following categories:

- Participation in public hearings

- Environmental assessment and substituted review panels under the Canadian Environmental Assessment Act

- Indigenous consultation

Terms and conditions (T&Cs) – 2010

T&Cs for the Grants and Contributions Program were developed and approved.

Funding Review Committee (FRC) – 2011

An independent FRC was established to provide an expert panel review of PFP applications, and recommendations on funding eligibility.

| 2011-2012 | 2012-2013 | |

|---|---|---|

| Actuals | $86,252 | $105,601 |

| Number of Recipients | 10 | 6 |

Second row 2013-2015: “Improve the PFP”

Risk Management – 2013

A PFP risk management model was developed and implemented

PFP processes – 2013

PFP procedure documents were developed in the CNSC Management System.

Program expansion – 2013

Management Committee (MC) members approved 2 further categories in addition to the original 3 categories described in the TB submission. According to the record of decision, this was done as both new categories are linked to Commission proceedings. The following categories were added:

- Support meetings with Indigenous groups on matters of regulatory concern

- Participation in CNSC targeted studies and monitoring.

CNSC web page – 2014

The web page was updated in order to give the public direct access to PFP guides and templates.

| 2013-2014 | 2014-2015 | |

|---|---|---|

| Actuals | $282,878 | $60,863 |

| Number of Recipients | 22 | 41 |

Third row 2015-2019: “Update the PFP”

Evaluation & audit reports – 2015

A strategic evaluations and internal audit were completed (covering 2011-14).

Program expansion – 2016

MC members approved funding for the following additional categories:

- Review of discussion papers, regulatory documents and regulations

- Long-term Indigenous engagement meetings and activities

- Participation of Indigenous communities in environmental monitoring, including the Independent Environmental Monitoring Program

Feedback – 2018

MC members requested feedback following Commission proceedings, including reporting on the value of the interventions receiving funding. The PFP is responsible for facilitating this process, and for documenting it in a value-added report.

MOU with impact Assessment Agency of Canada (IAAC) – 2019

With the creation of the IAAC and the Impact Assessment Act, processes were developed to enable the CNSC and IAAC to work together. The MOU outlines guidance for participants to allow a single process for integrated impact assessments.

| 2015-2016 | 2016-2017 | 2017-2018 | 2018-2019 | |

|---|---|---|---|---|

| Actuals | $170,760 | $233,541 | $589,367 | $853,035 |

| Number of Recipients | 13 | 66 | 59 | 54 |

Fourth row 2020-2021: “Current Status”

PFP demand – 2020

The PFP exceeding its funding authorities for the first time. It was forecasted in 2018 that the PFP would go over budget due to increased demand in future years.

IPRMC – 2020

Quarterly updates to the Integrated Planning and Resource Management Committee (IPRMC) Prior to these IPEMC updates, the PFP presented an annua update to Management Committee (2013-2018).

Future planning – 2020

The CNSC is looking at a new finding program that would support enhancing collaboration and capacity with Indigenous groups outside of a formal regulatory process.

Trust and reconciliation strategies – 2021

These strategies focus on building trust and on Indigenous reconciliation (including outreach and engagement at Commission proceedings). The PFP supports these strategies as a mechanism for enhancing participation at Commission proceedings.

| 2019-2020 | 2020-2021 | |

|---|---|---|

| Actuals | $1,037,265 | $1,109,137 |

| Number of recipients | 88 | 86 |

Appendix C Categories of PFP Funding Activities

| Funding activity | Source of activity | Reason for offering funding | What goes to the Commission |

|---|---|---|---|

|

1) Funding category: Project-specific funding |

|||

| Licensing renewal / amendment | 2010 TB submission |

|

Intervention from the funding recipient (written and/or oral). |

| Regulatory oversight reports (RORs) | 2010 TB submission |

|

Intervention from the funding recipient (written and/or oral). |

| Environmental assessments (EAs) | 2010 TB submission |

|

CNSC staff’s EA reports have a section listing and summarizing all the consultation activities supported through the PFP. The Commission also receives comments from the public and Indigenous groups on the draft environmental impact statement, as well as interventions from the funding recipients (written and/or oral). |

| Review of CNSC discussion papers | 2016 PFP expansion |

|

Intervention from the funding recipient (written and/or oral) or comments on the discussion paper, which are summarized and provided to the Commission (through a Commission member document (CMD) or presentation to the Commission by CNSC staff). |

|

Review of regulatory |

2016 PFP expansion |

|

Intervention from the funding recipient (written and/or oral) or comments on the regulatory document, which are summarized and provided to the Commission (through a CMD or presentation to the Commission by CNSC staff). |

|

2) Funding category: Funding for general matters of regulatory interest |

|||

| Participation in meetings with CNSC staff on topics of regulatory interest | 2013 PFP expansion |

|

Engagement activities supported through the PFP are summarized in a CNSC staff CMD, ROR, EA report, presentation or other reporting mechanism to the Commission. |

| Long-term Indigenous engagement meetings and activities | 2016 PFP expansion |

|

These engagement activities and the development of the ToR are conducted at the direction of the Commission and are in relation to and in support of Commission proceedings. Engagement activities supported through the PFP are summarized in a CNSC CMD, ROR, EA report or other reporting mechanism to the Commission. |

| Participation in targeted studies or monitoring | 2013 PFP expansion |

|

The study report and related data and information are summarized in a relevant CNSC CMD, EA report or other reporting mechanism. The full study report is also submitted to the Commission as part of a relevant proceeding, where appropriate. |

| Participation of Indigenous communities in environmental monitoring, including the Independent Environmental Monitoring Program (IEMP) | 2016 PFP expansion |

|

Engagement activities in relation to the CNSC’s IEMP sampling campaigns supported through the PFP are summarized in a CNSC staff CMD, ROR, EA report, presentation or other reporting mechanism to the Commission. |

Appendix D Financial Data

The following chart demonstrates the increase in demand for the PFP, from its creation in 2011 to present.

.png/object)

Text version

| FY | Actual | Number of Recipients |

|---|---|---|

| 2011-2012 | $86,252 | 10 |

| 2012-2013 | $105,601 | 6 |

| 2013-2014 | $282,878 | 22 |

| 2014-2015 | $60,863 | 41 |

| 2015-2016 | $170,760 | 13 |

| 2016-2017 | $233,541 | 66 |

| 2017-2018 | $598,367 | 59 |

| 2018-2019 | $853,035 | 54 |

| 2019-2020 | $1,037,265 | 88 |

| 2020-2021 | $1,109,137 | 86 |

Presentation of PFP recipient categories:

.png/object)

.png/object)

The tables below demonstrate the percentage of recipients within the PFP categories by fiscal year: 2019–20 and 2020–21

| 2019-20 | |||

|---|---|---|---|

| Designated group | % of funding actuals | % of recipients | No. of recipients |

| Indigenous groups | 76% | 65% | 57 |

| Non-governmental organizations | 22% | 31% | 27 |

| Individuals/Academics | 2% | 4% | 4 |

| Total | 100% | 100% | 88 |

| 2020-21 | |||

|---|---|---|---|

| Designated group | % of funding actuals | % of recipients | No. of recipients |

| Indigenous groups | 83% | 60% | 52 |

| Non-governmental organizations | 14% | 29% | 25 |

| Individuals/Academics | 3% | 11% | 9 |

| Total | 100% | 100% | 86 |

Source: Developed by the PFP

Appendix E ACRONYMS

The following table presents the acronyms used in this document.

| CMD | Commission member document |

| CNSC | Canadian Nuclear Safety Commission |

| EA | environmental assessment |

| ERP | Enterprise Risk Profile |

| FAD | Finance and Administration Directorate |

| FRC | funding review committee |

| IAA | Impact Assessment Act |

| IAAC | Impact Assessment Agency of Canada |

| IA | impact assessment |

| IEMP | Independent Environmental Monitoring Program |

| IPRMC | Integrated Planning and Resource Management Committee |

| ISRD | Indigenous and Stakeholder Relations Division |

| LS | Legal Services |

| MC | Management Committee |

| NSCA | Nuclear Safety and Control Act |

| PFP | Participant Funding Program |

| RAP | Regulatory Activity Plan |

| ROR | regulatory oversight report |

| SPD | Strategic Planning Directorate |

| T&Cs | terms and conditions |

| TB | Treasury Board |

| ToR | terms of reference |

Footnotes

- Footnote 1

-

Treasury Board of Canada Secretariat. InfoBase Glossary. Retrieved from: https://www.tbs-sct.gc.ca/ems-sgd/edb-bdd/index-eng.html#glossary

- Footnote 2

-

Treasury Board of Canada Secretariat. Government of Canada budgets and expenditures. Retrieved from: https://www.canada.ca/en/treasury-board-secretariat/services/planned-government-spending/budgets-expenditures.html

- Footnote 3

Page details

- Date modified: